You business continuity and success rides on your defence against liabilities – real or perceived. It i not uncommon for a company to be sued for a liability such as a person slips and falls in your retail store, your apprentice plumber knocks out a pipe and floods a home, or someone starts a cancel culture campaign (libel or slander) against your business which results in loss of business income.

CGL insurance enables you to continue your normal operations while dealing with real or fraudulent claims of negligence or wrongdoing. CGL policies also provide coverage for the cost to defend and settle claims.

Two main types of risk

Depending on the type of business you are in – there are generally two main types of risks. The risk of being liable for providing deficient, shoddy or incomplete work or products, and second, the risk of being liable for bodily injury or property damage resulting from providing inferior work or products.

You need Commercial General Liability Insurance if:

You have an office space or clients visit you at home.

You visit your client’s office space or home.

You have staff who conduct business off-site.

The only way to effectively protect the assets of your business is to carry adequate Commercial General Liability (CGL) Insurance coverage. CGL protects your business from damages caused by bodily injury or property damage for which your business is found to be legally liable.

What Does CGL Cover?

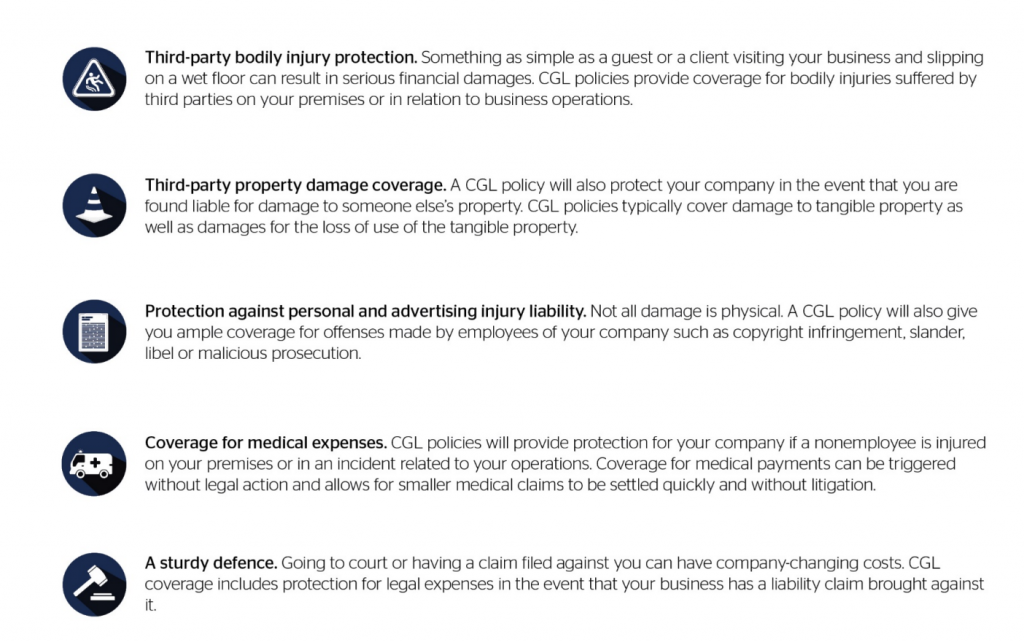

A typical CGL policy provides coverage for claims of bodily injury or other physical injury, personal injury (libel or slander), advertising injury and property damage as a result of your products, premises or operations, and can be offered as a package policy with other coverages such as property, crime, automobile, etc. As a safeguard against liability, CGL enables you to continue your normal operations while dealing with real or fraudulent claims of negligence or wrongdoing. CGL policies also provide coverage for the cost to defend and settle claims. Here is more detail about what a typical CGL policy may cover:

Automatic additional insured – Coverage is provided for written contracts, agreements and permits.

Personal and advertising injury – Protects against offences made by you or your staff during the course of business, such as libel, slander, disparagement or copyright infringement in advertisements.

Defence costs – Provides coverage for legal expenses for liability claims brought against your business, regardless of who is at fault.

Medical expenses – Provides coverage for medical expenses if someone is injured on your premises or by your products. For example someone attending a seminar at your office slips and breaks an ankle. The CGL policy will cover the medical expenses as per the policy wordings.

Occupiers and operations liability – Provides coverage for bodily injury and property damage sustained by others on your premises or in conjunction with your business operations.

Products Liability – Provides coverage for bodily injury and property damage sustained by others as a result of your products. For example a customer suffers from severe food poisoning after dining at your restaurant. The customer successfully sues you for bodily injury. Your CGL policy covers the medical expenses and legal fees.

How much coverage does your business need?

The amount of coverage that your business needs depends on three factors: where you operate your business, the type of products you manufacture and the perceived risk.

Type of product manufactured – If you manufacture a dangerous product -such as chemicals or fireworks, you may want to carry higher limits of liability.

Perceived risk – Consider the amount of risk associated with your business operations and functions. For instance, if you manufacture heavy equipment, you would generally need more coverage than another company that designs puzzles.

Premises and operations liability – If you operate in a province or area that has a reputation for rewarding high damages, then you may wish to purchase higher limits of liability.

Other ways to protect your business, in addition to CGL

-

- Establish a high standard for product quality control at your organization.

- Keep all company records up to date and accurate.

- Train your employees thoroughly and properly.

Ask Reliance Insurance Agencies, Ltd. for safety and compliance information.

Remember, you can purchase an Umbrella Liability policy to help achieve the desired limit of liability.

Resources for Defence Against Liabilities

Reliance Insurance: Umbrella Insurance

More information on commercial insurance from Economical

Reliance Insurance supports clients across Canada through a national network of offices and globally through our broker network partners.